FTLife社の積み立てリバース モーゲージ年金 / On Your Mind

- 契約している証券に予め年金用途のモーゲージ機能を付けられる、まったく新しいオフショア年金保険

- 通常の終身保険とは異なり、死亡保障額以上の金額をリタイヤ後の年金として予め本人にキャッシュアウト

- オンショアやオフショア問わずどこでも年金として受け取ったものは完全に非課税区分

- リタイヤ前の万が一の保障とリタイヤ後の生活保障を兼備

- 異なる受益者に異なる受取方法の設定可能

- 香港の保険情報比較サイトでは終身貯蓄型生命保険の死亡保障ランキングにおいて当該プランは、通年ランキング第1位

- 1. Policy Reverse Mortgage Programmeとは

- 2. ライフステージごとニーズに合わせたプラン A Plan to Meet Your Needs Before & After

- 2.1. 安心して年金生活を送るための「リバースモーゲージ機能」搭載 Built-in Policy Reverse Mortgage Function for you to enjoy annuity with total peace of mind

- 2.2. 重度認知症給付金で逆境を乗り切る Severe Dementia Benefit supports you through the time of adversity

- 2.3. ご家族に最適な死亡保険金の支払い方法を選択可能 Flexible Death Benefit Settlement Option which tailor the most suitable arrangement for your family

- 2.4. Built-in Policy Reverse Mortgage Function for you to enjoy annuity with total peace of mind

- 2.5. Flexible Death Benefit Settlement Option which tailor the most suitable arrangement for your family

- 2.6. Severe Dementia Benefit supports you through the time of adversity

- 3. 見積例 35才自営業者のAさん

- 4. 保障詳細 Benefit Details

Policy Reverse Mortgage Programmeとは

FTLife社が2020年業界初めて上市した当該プランOn Your Mindによって、海外投資家もPolicy Reverse Mortgage Programme(証券担保ローンのリバースモーゲージ計画)を購入できるようになりました。

経験豊富な海外投資家の方の中にはPolicy Reverse Mortgage Programme/保単逆按計画、直訳すると保険証券の逆担保なる投資商品をなんとなく聞いたことがある方もいらっしゃるのではないでしょうか。

日本で一般的なリバースモーゲージは自宅を担保にした融資制度

日本では大手都銀の商品として、自宅の不動産を担保に供するリバースモーゲージ型住宅ローンであれば、聞いたことがあるかもしれません。

Mortgageという意味は抵当や住宅ローンという意味で使われる言葉でLoanと同じ意味で使われることもあります。さて、一般的に不動産を所有している方が物件を担保に事業資金やリフォーム費用などの用途として、銀行から不動産担保ローンの融資を組むことが往々にあると思います。一括で受け取った融資額を月々返済していき、最終的に借入残高がなくなるのが通常でしょう。

その通常の不動産担保ローンと異なり、リバースモーゲージ型住宅ローンは、毎月、あるいは一括で借入れ(ここは普通のローンと同じ)、ただ、返済時期がリバースである旨の特約/条件を付けた契約を銀行と結びます。具体的に言うと、その返済方法と時期は、借主が最後(自分が死亡後)になった条件が発生すると、不動産売却による返済を行うことを予め定めることにより、最後に借入の元本をまとめて返済する仕組みとなりまます。なのでReverse(逆になる)という名称がつけられています。

元本の返済時が"将来"なのか"今"なのか、という違いがあるので、対象となる担保物件を死後には手放す形に抵抗感の無い方に好まれる傾向にあると言えます。一つの考え方として、子供が一生懸命働いて分に応じたものを得たほうが幸せな人生を送れるよう、財産を子供に残す必要はないと思っているなど。

香港では一歩進んでPolicy Reverse Mortgage Programme

金融都市の香港では日本より平均寿命が長く、リタイヤに備えた財務管理のニーズが増大してききました。その折2019年、公社であるHKMC/香港按揭證券有限公司が香港居民を対象に生命保険証書を物的担保にして、年金を借り入れることができるようにしました。これにより、不動産ではなく、しっかり積み立てた投資した証券の所有者が、Policy(証券)を担保に年金として保険会社からローンを組めむことができるようになりました。

ライフステージごとニーズに合わせたプラン A Plan to Meet Your Needs Before & After

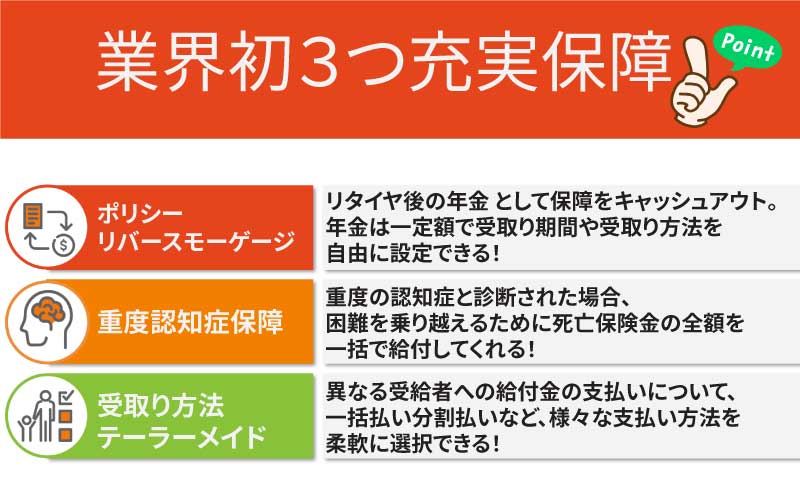

働き盛りの時は家族を守るために、退職後は自分とパートナーのために豊かな生活を送るために、それぞれのライフステージで必要な保障は異なります。このようなニーズにお応えするために、FTLifeでは 従来の生命保険の常識を覆す、全く新しい保険プランOn Your Mind(以下、本プラン)をご案内致します。従来の生命保険の常識を覆すものです。包括的な生命保険に加えて、市場初となるリバースモーゲージ機能を内蔵しています。そのため保険金を年金として引き出し老後の生活資金に充てることができます。大切な人へのプレゼントとして、また、老後の安定した収入のために。本プランは、3つの業界初メリットがあるオンマインド保険プランあなたのライフプランを柔軟にカスタマイズする一助になるはずです。

働き盛りの時は家族を守るために、退職後は自分とパートナーのために豊かな生活を送るために、それぞれのライフステージで必要な保障は異なります。このようなニーズにお応えするために、FTLifeでは 従来の生命保険の常識を覆す、全く新しい保険プランOn Your Mind(以下、本プラン)をご案内致します。従来の生命保険の常識を覆すものです。包括的な生命保険に加えて、市場初となるリバースモーゲージ機能を内蔵しています。そのため保険金を年金として引き出し老後の生活資金に充てることができます。大切な人へのプレゼントとして、また、老後の安定した収入のために。本プランは、3つの業界初メリットがあるオンマインド保険プランあなたのライフプランを柔軟にカスタマイズする一助になるはずです。

以下では業界初3つの機能の詳細を見ていきます。

安心して年金生活を送るための「リバースモーゲージ機能」搭載 Built-in Policy Reverse Mortgage Function for you to enjoy annuity with total peace of mind

老後の生活に不安を感じている方のために、従来の生命保険の常識を覆す「リバースモーゲージ機能」を新たに搭載しました。

被保険者の死亡後、保険金受取人に支払われる死亡保険金に加えて、老後の生活に必要な年金を事前に引き出すことができます。年金は一定額で、年金受取期間や年金支払方法を自由に設定することができます。また、年金期間中の年金支払いを停止したり、停止後の年金支払いを再開したりすることも、書面で申し込むことができます。

さらに停止後に再開することができるほか、保険金を年金として引き出しても、保険金額には影響しません。

すなわち本プランで様々なライフステージにおけるお客様のニーズに合わせた柔軟な対応が可能となり、将来の理想的なリタイアメントライフを安心して計画し、大切な家族に万全の保障を与えることができるのです。

重度認知症給付金で逆境を乗り切る Severe Dementia Benefit supports you through the time of adversity

被保険者が不幸にして重度の認知症と診断された場合、その困難を乗り越えるために、死亡保険金をお持ちのご主人に全額を一括でお支払いし、死亡保険金を事前にお支払いします。

ご家族に最適な死亡保険金の支払い方法を選択可能 Flexible Death Benefit Settlement Option which tailor the most suitable arrangement for your family

不幸にして被保険者が死亡した場合、異なる受給者への給付金の支払いについて、一括払いや分割払いなど、様々な支払い方法を柔軟に選択することができます。

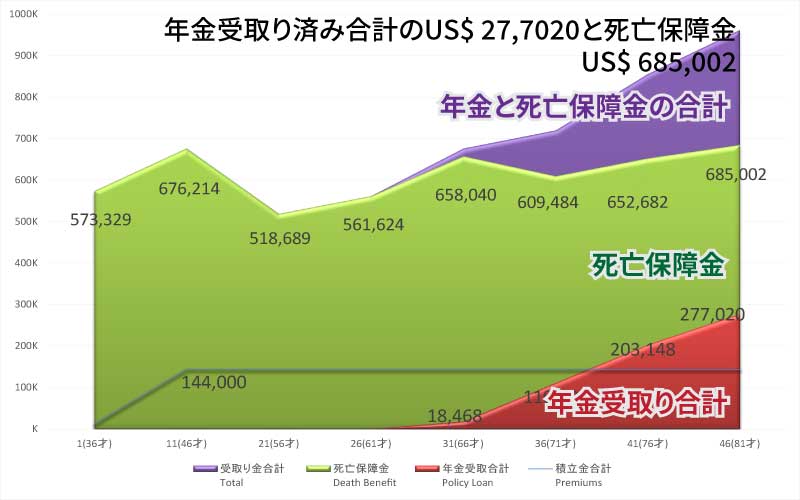

見積例 35才自営業者のAさん

35才自営業者のAさん、リタイヤ後の貯蓄と生命保険の保障の両方に備えたい。

理由は日本の年金に加入しているももの65才以降から本当に受け取れるかどうか疑問がある上に年金額が少なく日本円では急激な円安とインフレリスクが大きいすぎるので確実に受け取れ、しかも外貨の年金も用意しておきたいと思った。

また、生命保険機能として、リタイヤ前に万が一死亡の際、大事な家族の経済的支えがなくなる憂いや年金を積み立てても死亡時には遺族への相続ができないことや遺族年金も不十分であることを認識しているので、死後に子供やパートナーに最高のものをどうしても残してあげたいと思うに至った。

積み立て金額と期間

頑張って毎月US$1,000を12年間、積み立てを開始。12年後には合計US$144,000(1000米ドル/月×12カ月×12年)を積み立てることになります。

ケース1: ポリシーリバースモーゲージの年金受け取りと、その後の死亡保障で支払い済み保険料の6倍以上受け取れる

66才の年から80才までの15年間毎月US$1,539を合計27,7020(1,539米ドル/月×12カ月×15年)をモーゲージの年金として受け取った上に平均寿命の81才で死亡。死亡保障金でモーゲージは完済の上、残金の死亡保障金は遺族へ、その受け取り金はUS$685,002。

この場合、支払い済み保険料のUS$144,000に対して予測給付の受け取り分は1億円近いUS$27,7020+US$685,002=US$962,022となり、668%(962,022/144,000×100%)

ケース2: 11年目に仮にAさんが地震などの災害で死亡しまった場合

受取可能額は本来の死亡保障額の100%と、早期に亡くなってしまったので保障額に対して追加の死亡保障50%と追加のの災害死亡保険金をお支払い。支払い済総保険料US$144,000に対して保障総額はなんと1.6億円程度のUS$1,352,428米ドル(約1,000%)。

追加の死亡保障と災害死亡保険金とで本来の死亡保障の200%を給付 Extra Death Benefit and Extra Accidental Death Benefit

突然の生活の変化は、家族に大きな経済的負担を強いることになります。被保険者が契約後20年以内に不幸にも次のような事態に陥った場合、追加で次のような保険金をお支払いします。

- 被保険者が不幸にしてお亡くなりになったり、重度の認知症や末期疾患と診断された場合

保険金額の50%を上限として、ご契約者が事前に選択された所定の死亡給付金受取方法により追加の死亡給付金として個々の受取人にお支払いします。重度の認知症や末期疾患の医療費の負担を軽減するために、死亡臨時給付金の保険金額の50%までを一括してご契約者にお支払いします。 - 被保険者が180日以内に不幸にして81歳になる前に災害により死亡した場合

上記の追加死亡保険金とは別に、不測の経済的負担を軽減するために、保険金額の50%を限度として追加死亡保険金が保険金受取人に支払われます。

証券年度が20年以内に被保険者が死亡や末期疾病、重度認知症と診断されると下記のテーブルの追加の死亡保障を受取れます。

| 証券年度 | 追加保障% |

|---|---|

| 1年目~11年目 | 50% |

| 12年目 | 45% |

| 13年目 | 40% |

| 14年目 | 35% |

| 15年目 | 30% |

| 16年目 | 25% |

| 17年目 | 20% |

| 18年目 | 15% |

| 19年目 | 10% |

| 20年目 | 5% |

| 21年目以降 | 0% |

災害を原因として180日以内に死亡すると下記のテーブルの追加の災害死亡保障の受取ができます。ただし、証券年度が20年目まで且つ被保険者 は81歳未満に限ります。

| 証券年度 | 追加保障% |

|---|---|

| 1年目~11年目 | 50% |

| 12年目 | 45% |

| 13年目 | 40% |

| 14年目 | 35% |

| 15年目 | 30% |

| 16年目 | 25% |

| 17年目 | 20% |

| 18年目 | 15% |

| 19年目 | 10% |

| 20年目 | 5% |

| 21年目以降 | 0% |

保障詳細 Benefit Details

基本情報 Basic Information

| 保険期間/Policy Term | 終身/Whole life |

|---|---|

| 証券通貨/Policy Currency | 米ドル/US dollars |

| 保険料支払い方法/Premium Mode | 年払いや半年払い、月払い/Annual, semi-annual, and monthly payment |

| 保険料支払期間/Premium payment period | 発行年齢/Issue age |

|---|---|

| 6年(一括前払いのオプションあり)/6 years (an option for a lump sum prepayment) | 生後15日から70歳まで/From 15 days to 70 years of age |

| 12年/12 years | 生後15日から65歳まで/From 15 days to 65 years of age |

| 20年/20 years | 生後15日から60歳まで/From 15 days to 60 years of age |

| 25年/25 years | 生後15日から55歳まで/From 15 days to 55 years of age |

Policy Reverse Mortgage Loan

被保険者が生存してプランが有効である間、保険契約者は所定の書式で請求を行い、組み入れられているPolicy Reverse Mortgage Loanの機能を行使してローンを申し込むことができます。定期年金は、ご指定の年金期間と支払方法に応じて、以下のように一定額をお支払いします。

| 年金期間/Annuity period | 15年,20年,30年,40年(最後の年金支払いは、被保険者が100歳に達した契約応当日以前に支払われなければなりません) |

|---|---|

| 年金の支払い方法/Annuity Payment mode | 月間や半年間、年間/Monthly / semi-annual / annual |

| 1回あたりの最低年金額支払額/Minimum Annuity Payment amount per installment | Monthly: 125 |

| Semi-annual: 750 | |

| Annual: 1,500 | |

| 適格性/Eligibility |

以下の4つの条件をすべて満たす必要があります。 1. Policy Reverse Mortgage Loanは、以下の項目の日付以降に取得されること。 (i)~(iii)のいずれか新しい方。 i) 被保険者が60歳になったとき、または ii) 本プランの保険料終了日、または iii) 15回目の契約記念日、および 2. 85歳に達した被保険者の誕生日以前に取得されたもの、および 3. 取得時に本プランの保険料が全額払い込まれており、債務がないこと。 4. 本プランの被保険者は、リバースモーゲージを取得した時点で65,000米ドル以上であること。 |

| 費用/Charges |

1. Policy Reverse Mortgage Loan金利 最初の10年間のローン金利はローンの総額に基づいて金利が請求される時点での当社が指定する銀行が発行するプライムレート※から3%を差し引いた値(P-3%以上0%以下)で計算されます。 最初の10年間Policy Reverse Mortgage Loanを取得した後、ローン金利はオーナーに通知することなく当社が随時決定しますが、常にプライムレート※を超えないことを条件とします。 ※当社は現在、HSBC香港が公表しているプライムレートを参照していますが、この指定銀行は契約者に通知することなく当社が随時変更することがあります。 2.ローンの年間料金 死亡保険金および臨時死亡保険金の合計額に、0.1%~0.5%の範囲で設定された利率を乗じた金額が、年額ローン期間中に毎年前払いしていただきます。本契約のPolicy Reverse Mortgage Loanをご利用になる前に、この金利は参考値であり保証されるものではありません。実際の利率は、リバースモーゲージ契約締結時に決定され、固定され保証されます。年間ローン料金の支払い期間中に、被保険者が死亡または重度の認知症や末期疾患と診断された場合、支払われた年間ローン料金の総額の50%を所有者に返金します。 3. 融資手数料 融資手数料は、毎月の契約応当日に本契約のPolicy Reverse Mortgage Loanの総額(返済額がある場合はそれを差し引いた額)の年率1%に相当する額を前払いで請求します。 上記のすべての費用とその利息はPolicy Reverse Mortgage Loanの元本に算入されます。 |

| 特記事項/Special Notes |

本プランでは、一度だけPolicy Reverse Mortgage Loanを利用することができます。 • 年金支払可能額は、被保険者の年齢や年金期間等の諸条件に応じてFTLifeが決定します。 • 年金受取期間中にPolicy Reverse Mortgage Loanを停止し、停止後に再開することを書面でお申し込みいただけます。 • 契約者は年金期間中、非保証のボーナスの現金価値を引き出すことはできません。年金期間終了後はPolicy Reverse Mortgage Loanやプランに基づく負債を最初に控除することを条件に、無保証のボーナスの現金価値(もしあれば)を引き出すことができます。 • 一部解約後、保証現金価値や非保証ボーナス(もしあれば)、受取れなかった年金支払額は比例して減少する。また、Policy Reverse Mortgage Loanも同様に比例して返済されます。 • 契約者は、いつでもPolicy Reverse Mortgage Loanの全部または一部を返済することができます。 |

Remarks:

1. Cooling Off Right

If you wish to exercise your cooling-off right, you can cancel the policy and obtain a refund of premium and levy paid by giving a written notice to us. Such notice must be signed by you and submitted to our office at 7/F, NEO, 123 Hoi Bun Road, Kwun Tong, Kowloon within 21 calendar days immediately following the day of delivery of the policy or the Cooling-off Notice to you or your nominated representative (whichever is the earlier). The Cooling-off Notice should inform you of the availability of the policy and expiry date of the cooling-off period.

2. Grace Period

We shall allow a grace period of 31 days after the premium due date (the “Grace Period”) for payment of each premium (other than the first premium) during which this Policy will remain in force. If any premium is not paid on or before its due date, that premium is in default. If that premium remains unpaid at the end of the Grace Period, unless that premium is paid by the automatic premium loan, this Policy terminates as from the last premium due date. We shall not be liable to pay any benefit arising from any event occasioned during the Grace Period

unless the overdue premium is paid before the end of the Grace Period.

3. Key Product Risks

i) Non-guaranteed Benefits

Dividend / Bonuses are not guaranteed. We will review the dividend / bonuses regularly, and the actual dividend / bonuses can be different

from those shown in the benefit illustration.

ii) Termination

The coverage of the Insured under the Plan shall be automatically terminated upon the earliest occurrence of the following circumstances:

1. any premium under this Policy remains in default at the end of the Grace Period; or

2. the amount of indebtedness from policy loan equals to or exceeds the sum of the guaranteed cash value and the cash value of

accumulated reversionary bonuses (if any); or

3. the death of the Insured; or

4. the Terminal Illness Benefit is paid or payable; or

5. the Severe Dementia Benefit is paid or payable; or

6. this Policy is fully surrendered.

Any Policy Reverse Mortgage Loan shall be repaid in full upon the termination of the policy. Even if the benefit or the surrender payment is insufficient to fully repay the Policy Reverse Mortgage Loan, the Owner is not required to settle the difference upon the termination of the Plan.

The key items of policy termination are listed above. Please refer to the policy provisions for the full list of policy termination.

iii) Policy Reinstatement

If this policy terminates due to non-payment of any premium, it may be reinstated subject to the written request for reinstatement made by you within 2 years from the due date of the premium in default and meet our administrative regulations at that time.

Please refer to the policy provision for details of reinstatement.

iv) Inflation Risk

When you review the values shown in the benefit illustrations, please note that the cost of living in the future is likely to be higher than it is today due to inflation. In that case you will receive less in real terms even if we meet all of our contractual obligations under the policy.

v) Surrender Provisions

After this policy has acquired a cash value, you may surrender this policy with a written notice to us, subject to the prevailing administrative rules of the Company. Please refer to the policy provisions for details of policy surrender.

4. Other Key Product Risks

• “On Your Mind” Insurance Plan is issued in US dollar. The premiums received by us in a currency different from your policy currency will be converted to the policy currency at the prevailing exchange rate determined by us from time to time with reference to market rates. All monies payable under your policy will be paid in Hong Kong dollars, or in the policy currency upon your request. The amount payable by us in a currency different from your policy will be converted at the prevailing exchange rate determined by us from time to time with reference to market rates. Therefore, it may be subject to foreign exchange risks in the process of currency conversion.

• “On Your Mind” Insurance Plan is an insurance policy issued by us. The insurance benefits are subject to the Company’s credit risks.

5. Claim Procedure

You must notify us by submitting the appropriate forms and relevant proof within 90 days of the date of unequivocal diagnosis of Terminal Illness / Severe Dementia if you wish to make a claim. You can get the appropriate claim forms from your financial consultant or call the FTLife customer service hotline on 2866 8898.

6. Suicide Clause

If the Insured commits suicide within 1 year from (i) the policy effective date; or (ii) the last date of reinstatement (whichever is later), our liability will be limited to the refund of total premiums paid less any type of bonus withdrawal, claims, indebtedness or Policy Reverse Mortgage Loan. If the Insured commits suicide within 1 year from the effective date of any increase in sum insured or any subsequent addition of plan, our liability in respect of that increase of sum insured or addition of plan will be limited to the refund of the corresponding increment of premium paid less indebtedness or Policy Reverse Mortgage Loan, any type of bonus withdrawal and claims which have been paid by us in respect of the relevant increase of sum insured or addition of plan.

7. Exclusions

i) Severe Dementia Benefit / Terminal Illness Benefit

We will not pay any Severe Dementia Benefit / Terminal Illness Benefit under the Plan if the Insur ed is diagnosed with Severe Dementia / Terminal Illness that is caused directly or indirectly, wholly or partly, voluntarily or involuntarily by self-inflicted injury,including without limitation, suicide or any attempt to do so, while sane or insane; or c onsumption of or being under the influenc e

of alcohol, poison, medication, drugs or sedatives unless prescribed by a Medical Practitioner.

ii) Extra Accidental Death Benefit

We will not pay any Extra Accidental Death Benefit under the Plan if the death of the Insured is caused directly or indirectly, wholly or partly, voluntarily or involuntarily by or is resulted from any of the following occurrences:

1. War, declared or undeclared, revolution or any warlike operations;

2. Violation or attempted violation of the law or resistance to arrest;

3. Engaging in services in armed forces in times of declared or undeclared war or while under orders for warlike operations or

restoration of public order;

4. Entering, exiting, operating, being transported, or in any way engaging in air travel except as a fare paying passenger in any aircraft operated by a commercial passenger airline on a regular scheduled passenger trip over its established passenger route;

5. Childbirth, miscarriage, pregnancy, or any connected complications notwithstanding that such event may have been accelerated or induced by Injury;

6. Engaging in a sport in a professional capacity or where the Insured would or could earn income or remuneration from engaging in such sport;

7. Acquired Immune Deficiency Syndrome (AIDS), and/or any Illness or Injury commencing in the presence of a seropositive test for

Human Immunodeficiency Virus (HIV), and any related disease;

8. Self-inflicted injury including suicide or any attempt thereat while sane or insane and/or any event of consumption of or being under the influence of alcohol, poison, medication, drugs or sedatives unless prescribed by a Medical Practitioner;

9. Disease or infection (except diseases causing infections which occur due to an accidental cut or wound);

10. Poison, gas or fumes, voluntarily or otherwise taken, absorbed or inhaled, other than as a result of an Accident arising from a hazardous incident in relation to the Insured’s occupation.

iii) Waiver of Premium Benefit

We will not pay any Waiver of Premium Benefit under the Plan in any of the following situations:

1. If the total permanent disability of the Insured is caused directly or indirectly, wholly or partly, voluntarily or involuntarily by or is resulted from any of the following occurrences:

i. Self-inflicted injury, including suicide or any attempt to do so while sane or insane; or

ii. Use of narcotics unless taken as prescribed by a Medical Practitioner, or abuse of drugs and/or alcohol; or

iii. Violation or attempted violation of the law or participation in fight or affray or resistance to arrest.

2. Waiver of Premium Benefit arising directly or indirectly from the following Pre-existing Conditions:

i. A condition of the Insured for which medical advice, diagnosis, care or treatment was recommended or received before the

Policy Effective Date or any date of reinstatement (whichever is later); or

ii. Any sign or symptom of the Insured within a five-year period immediately preceding the Policy Effective Date or any date

reinstatement (whichever is later). And such sign or symptom would have caused an ordinary prudent person to seek medical

advice, diagnosis, care or treatment.

8. Dividend / Bonus Philosophy

• Premium income received from the Owner is invested in an investment portfolio to support the product groups determined by us according to the investment policy. The Owner participate in the financial performance of the Product Group through the dividends/bonuses declaration. The dividends/bonuses declaration may be affected by both past experience and future outlook for all the factors including, but not limited to, the following:

a) Investment returns: include both interest earnings and any changes in the market value of the asset allocated to this product.

Investment returns could be affected by fluctuations in interest income (both interest earnings and outlook of interest rate) and various market risks, including credit spread and default risk, fluctuations in equity price and currency price of the asset against the policy currency.

b) Surrender: include policy surrender, partial surrender and policy lapse experience; and the corresponding impact on investments.

c) Claims: include the cost of providing the Death Benefit and other insured benefits under the product.

d) Expenses: include both expenses directly related to the policy (e.g. commission, underwriting, issue and premium collection expenses) and indirect expenses allocated to the product group (e.g. general administrative costs).

• Future investment performances are unpredictable, and we aim to provide a more stable dividend payment/bonus distribution. We may spread out the gains and losses in the financial performance in a particular year over a longer period of time aim to smooth out the short-term volatility of dividend/bonus over the course of the policy term. When future investment performance is worse than expected, the Company’s shareholder may share less from the investment performance such that more may be allocated for dividend payment/bonus distribution, and vice versa.

• The Board, having regard to the advice of the Appointed Actuary and reviewed by Risk Committee which must include one independent non-executive director, will review and determine the dividend/bonus at least once a year. The declared dividend/bonus may be different from those illustrated in the relevant product information provided, e.g. benefit illustration. In case of any change in the actual dividend/bonus against the illustration or should there be a change in the projected future dividend/bonus, such change will be reflected in the Policy Anniversary statement and the benefit summary.

9. Investment philosophy, policy and strategy

• Our investment policy aims to achieve the targeted long-term investment results and minimizes volatility in investment returns over time.

It also aims to control and diversity risk exposures, maintaining adequate liquidity and manage the assets with respect to the liabilities.

• Our current long-term target asset allocation attributed to this product is as follows:

Target Asset Mix

Fixed income type securities

(Investment grade and non-investment grade) Equity-like assets

50% – 100% 0% – 50%

• Investment instruments include cash, deposits, investment grade and non-investment grade bonds, unrated bonds, listed equities,

exchange-traded funds or other structured products. Derivatives and other hedging instruments may be used to manage investment

risk at the Company’s decision based on its long-term market view and asset-liability positions. It should be noted that residual

investment risk may still exist after hedging.

• The asset portfolio also targets to provide diversification across different geographic regions (focus on the U.S., Europe and Asia Pacific markets) and industries to the extent the size of portfolio can support. Currency exposure of the underlying policies is mitigated by closely matching either through direct investments in the same currency denomination or the use of currency hedging instruments.

Furthermore, the asset portfolio is actively managed by investment professionals to closely monitor the investment performance.

• The investment strategy may be subject to change depending on the investment views and economic outlook. In case of any changes in the investment strategy, we will inform our Owners for any material changes, rationale for the change and any impact to the Owners.

You may

オフショア香港のFTLife社の商品のお申込みついて

FTLifeには香港でもっとも有名な保険会社。親会社は香港最大手の貴金属店の周大福やK11ショッピングモール、市バスなどを所有するNew World Development/新世界発展。つまり、香港を代表するコングロマリット(香港系財閥)の金融部門を担っている。2,800人以上のエージェントや独立した財務アドバイザーが在籍しています。

FTLifeの商品につき取り扱い商品

弊社取り扱いお勧め商品としては

- 積み立て資産承継貯蓄保険のRegent Insurance Plan 2 Premier

- 一括払い資産承継貯蓄保険のFortune Saver Insurance Plan Ⅱ

- 年金プランのIncomePro Annuity Plan

- 積み立て投信保険のOscar

- 一括支払い投信保険のLegend

- 積み立てリバース モーゲージ年金保険のOn Your Mind

| サポート内容抜粋 | 料金(HK$) |

|---|---|

| 商品のご案内 | 無料 |

| 住所や電話番号など各種変更手続き | 1,000/回 ※弊社の顧客は無料 |

| その他、各種手続きやトラブル解決や通訳 | お問合せください |

FTLife香港の基本情報 Fundamental information of FTLife Hong Kong

香港で最も知名度のある保険会社の一つです。アジア地域にグローバル金融サービスを提供しています。

世界の格付け機関から受けた推奨や高格付け(Fitch Ratings A-)は、F財務力の強さを表しています。FTLifeは多様な商品を提供し、将来設計や資産承継などあらゆる角度から顧客の資産をオフショアで保全します。

| 名称 | FTLife Insurance Company Limited / 富通保保険有限公司 又は単に FTLife |

|---|---|

| KOWLOON - FTL Prestige Service Centre | Suite 3106-09, 31/F, Tower 6, Gateway, Tsim Sha Tsui, Kowloon, Hong Kong |

| 営業時間 ※香港時間 | 月~金曜日: 9:00~19:00 土曜日: 9:00~13:00 |

| カスタマーホットライン/電話番号 | +852 2866 8898 |

| ホームページURL | https://www.ftlife.com.hk |

| csc@ftlife.com.hk | |

| 申請書等の送付先 | FTLife Kowloon Customer Service Centre 7/F NEO, 123 Hoi Bun Road, Kwun Tong, Kowloon, Hong Kong |