FTLife社の一括払い、資産承継貯蓄保険フォーチュンセーバー / Fortune Saver 2

- 一括払いで総保険料をなるべく抑え、堅実に安定した資産形成を実現

- 何度でも名義変更が可能(回数無制限)

- 80才でも加入できる上に、オフショア香港で保険契約内で譲渡可

- 現代の人生100年時代をもとに設計されているので、保障期間は128才まで

- 最大8%の高額割引特典あり

ポストコロナの世界では、個人国家を問わず経済秩序が大きく変化していくと予想されます。そんな中、ウィルスが身体を知らぬ間に蝕むように、苦労して得た資産を不動産をはじめ資産すべてを円建てポートフォリオを構築することは、非常に危険が多いと言えます。

ポートフォリオにマイナス金利で運用されている預貯金や国債の割合が多い方は、当該商品で外貨建ての財産をオフショアで自由に増やし、無駄なく大切な子や孫へ承継し、自身はもちろん子々孫々の繁栄にも大きな助けとなることでしょう。

- 1. FTLife社の貯蓄性の高い一時払い承継保険、Fortune Saver Insurance Plan Ⅱ

- 2. 何度でも名義変更可能(回数無制限)。しかも、新たな被保険者の128才まで自動延長 Unlimited changes of the insuredUnlimited changes

- 3. 保険契約の延長オプション(受益者へ)[3]Policy Continuation Option

- 4. 高額契約者には最大8%の割引[8] Large Size Discount up to 8%

- 5. 解約返戻金[7]や死亡保険金[6]の受取オプション Flexible Settlement Options

- 6. 追加の死亡保障金[4] Additional Accidental Death Benefit

- 7. フォーチュン セーバー2の詳細 At-a-Glance Table

FTLife社の貯蓄性の高い一時払い承継保険、Fortune Saver Insurance Plan Ⅱ

堅実に安定した資産形成を実現しつつ、早期引き出しがきる上、無期限で次世代への継承ができるオフショア保険ならではのメリットを享受できます。

解約返戻金(保証)のみでも損益分岐点は6年目 Guaranteed breakeven period as short as 6 years

保証されている解約返戻金のみでも損益分岐点は6年目。そのため早期に解約した場合でもリターンを享受することができます。

当該プランでは、自身の年金や子供の教育資金の捻出の助けになるよう引き出しも可能なので、老後の準備をしている方や子供の将来を考えている方にピッタリと言えます。

契約の保障期間は被保険者の128歳までとなっており、超長期的な資産形成の機会を提供し、Prudent-Progressive principleの攻守ともに備える資産戦略を実現してくれます。現金価値の保証とさらに年次配当金(非保証)[9]、終了時配当金[9]が提供されるので資産を案的的、継続的に成長させることができます。

契約と開始と同時に現金価値を維持 Enjoy cash value upon policy starts

解約返戻金の損益分岐点が4年目、保証されている解約返戻金のみでも損益分岐点は6年目となり、堅実に安定した資産形成を実現してくれます。

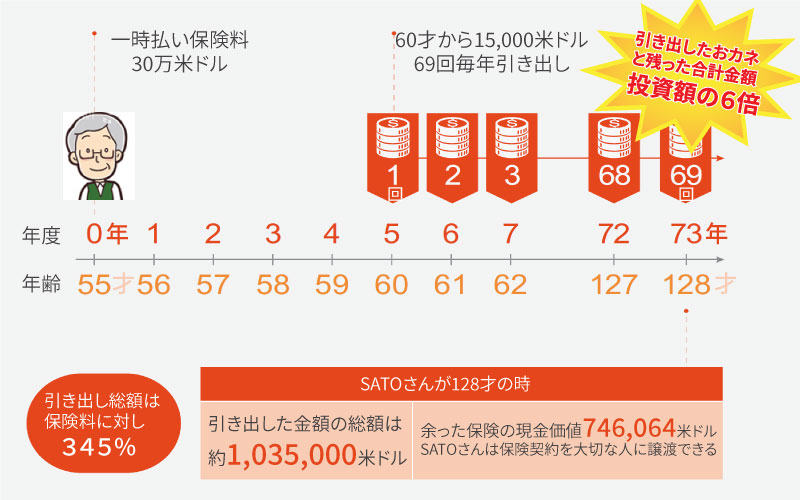

自分年金のための当該商品の見積り例

明るい未来のために自分で年金を作るSATOさん、55才のとき300,000.04米ドルを一括で払ったことを前提にしたライフプラン シミュレーションです。

55歳の時に30万米ドルの一時払いの保険料を支払い60歳で退職した後、128歳までは退職後の生活の足しに毎年1.5万米ドル(支払保険料総額の5%[5])を合計69回の100万米ドル以上を保険契約から引き出した。

学資保険として利用する場合の見積り例

大切なご子息SATOジュニアさん、10才、50,000米ドルを一括で払ったことを前提にしたライフプラン シミュレーションです。

子供が10才のときに将来の大学の学費と経済的に独立するまでの援助に用立てするつもりで5万米ドルのみ購入。大学4年間の学費の一部として賄えた上、周到に準備された子供への資産承継としても有効となった。

何度でも名義変更可能(回数無制限)。しかも、新たな被保険者の128才まで自動延長 Unlimited changes of the insuredUnlimited changes

証券発行の1年目以降から被保険者を何度でも変更できる[2]ので、被保険者の変更後の保障期間は、新たな被保険者が128歳になるまで延長されます。相続が3代続くと財産はなくなると言われる日本と異なり、長い年数は富を十分に蓄積させてくれるので、オフショア香港の保険契約内で無限に次の世代に渡すことができるのです。

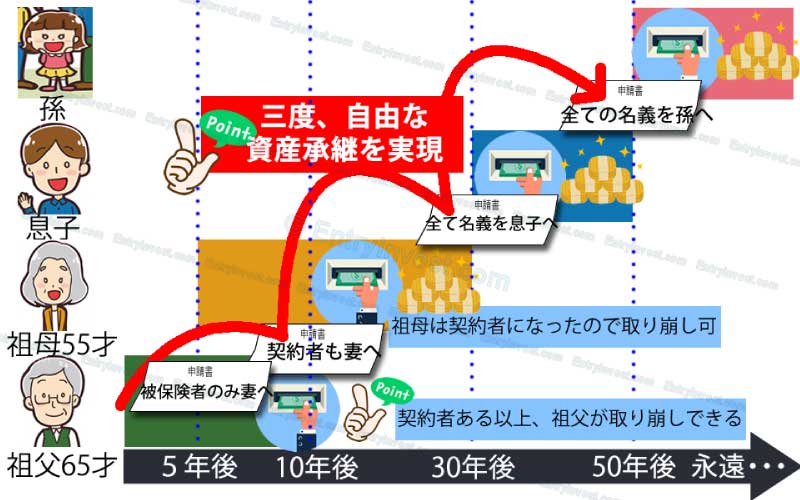

以下のイメージのモデルは、人生100年時代の老後の資金対策、それと計画的な相続や贈与に熱心な65才の祖父がいたとします。

上記のイメージは、5年後に祖母に権利の一部を与え10年後に完全に契約名義を含めて移譲。その後、祖母は20年間金利収入を得たものの名義を完全に息子に引継ぎ、さらに息子は20年後、祖父から見れば孫に自由に移譲を完了。

保険契約の延長オプション(受益者へ)[3]Policy Continuation Option

上記の被保険者の生前の名義変更[2]とは別に、「保険契約継続オプション[3]」を特別に用意されています。

被保険者が生存している間、保険契約者は受取人である受益者を指定することができますが、万が一名義変更前に被保険者が死亡した場合、受益者は新たな保険契約者となり、新たな被保険者となり得ます。保険契約は次の世代にオフショア保険内で引き継ぐことができます。保険期間は、新たに被保険者の128歳に調整されます。

高額契約者には最大8%の割引[8] Large Size Discount up to 8%

一定の保険料に達すると最大8%の高額契約の優待割引を受けることができます。安心して資産運用と保障プランを始められます。

| 対象となる一括保険料*(US$) | 高額契約割引率 |

|---|---|

| ≥ 300,000 | 8% |

| 100,000 –< 300,000 | 6% |

| 50,000 –< 100,000 | 4% |

| 対象となる一括保険料*(US$) | 高額契約割引率 | 高額契約割引金額 | 割引後の保険料 |

|---|---|---|---|

| 300,000 | 8% | 24,000 | 276,000 |

| 100,000 | 6% | 6,000 | 94,000 |

| 50,000 | 4% | 2,000 | 48,000 |

* 上記一括保険料は、大型割引前のものです。

解約返戻金[7]や死亡保険金[6]の受取オプション Flexible Settlement Options

死亡保険金と解約返戻金の受取頻度を毎月や半年、年払いで指定できるほか、残金に2%の金利(変動性)[10]が付与されます。

まとまったお金が必要なら一括受取り Full surrender Settlement

解約返戻金を一括で日本や香港の口座、小切手で受け取る方法です。メリットとしては一度にまとまった資金を準備できることがあげられます。「子供が海外の大学に入学するので外貨建ての資金が必要」、「海外移住のために資金が必要」等まとまった資金が必要な場合には、こちらの受取方法がおすすめとなります。

できるだけ多く受け取りたいなら年金受取り Regular payments

個人年金のように、毎月受け取りのように年金形式で受け取る方法です。10年や20年、30年にわたり毎月や半期、毎年ごと定期的な受け取りにできます。解約返戻金を年金のような形で年間1万米ドルずつ10年間(合計10万米ドル)受け取るといったことができます。そのため子供の大学の学費に利用する際などにも、非常に便利な受取方法となっています。

ただし、解約の場合、現金価値が5万米ドル以上で且つ契約から5年経過していた場合のみ当該年金受取りオプション利用可。

終了時配当金のロックインオプション[1] Terminal Dividend Lock-In Option

市場の変動から富を守るために、以下の終了時配当金ロックインオプション[1]のいずれかを申請して、終了時配当金[9]を年次配当金[9]の形で変換して蓄積するか、必要な時に撤回するかを選択することができます。変換された終了時配当金は保証付きとなり、安定したリターンをもたらしてくれます。また、変換された終了時配当を年間配当の形で積み立てて利息を得ることもできます。

- 自動ロックインオプション/Automatic Lock-In Optionを年次配当金[1]第15回目の契約日または被保険者が選択した定年退職年齢(55歳以上)に達した直後の契約日(いずれか遅い方)から、終了時配当金を年次配当金[9]の残額が30%になるまでの間、払込保険料総額を年次配当金[5]の8%を起算した額を、各契約日ごとに自動的に年次配当金を年次配当金[9]に換算します。

- 手動ロックインオプション/Manual Lock-In Optionを年次配当金[1] 15 契約日目から、ご希望の終身配当金を年次配当金[9]の一部を、ご指定の契約日に年間配当金9に転換することができます。終了時配当金を年次配当金[9]の10%以上を1回ごとに、合計60%まで転換できますが、転換の間隔は3年以上必要となります。

契約時に設定する必要はありません。契約後15年目が近づいてから社会情勢を見つつ、非保証部分がどのように増えているのかを見つつ、決めたらいいと思います。

追加の死亡保障金[4] Additional Accidental Death Benefit

事故により被保険者が最初の8年以内に死亡した場合、死亡給付金に加えて、支払われた保険料総額の100%[5]が受取人に支払われ、1人の被保険者につき最低1.5万米ドル、最高額15万米ドルが給付されます。事故死給付金は、80歳以下の被保険者にも適用されます。

フォーチュン セーバー2の詳細 At-a-Glance Table

当該商品、貯蓄性の高い一時払い承継保険、Fortune Saver Insurance Plan Ⅱをテーブルで以下のようにまとめます。

| 支払い頻度 | 一括/一時払いのみ 香港の銀行から引き落とし or 日本の銀行からの送金 or VISA/Masterカードで引き落とし |

|---|---|

| 加入年齢 | 出生15日から80歳まで |

| 保障期間 | 被保険者が128歳になるまで |

| 最低投資額 | US$10,000 |

| 死亡保障 | 75才以下: 105~110% 76才以上: 101% |

| 年次配当[9] | 契約期間中は、11年目から毎年配当(非保証)開始。以下のオプションがあります。 ⅰ)利息付き積立(デフォルトオプション) ⅱ)現金での支払い |

| 終了時配当[9] | 契約期間中は、1年毎に1年目の契約日から終了時配当金(非保証)開始。次のいずれかのタイミングで給付。 ⅰ)被保険者が死亡した場合 ⅱ)全部解約や一部解約 ⅲ)保険契約の満期日 ⅳ)自動手動ロックインオプションの実行時 |

Remarks:

1. You can apply changes between Automatic Lock-In Option/Manual Lock-In Option for unlimited times before exercising the “Terminal Dividend Lock-In Options”. Once the option has been exercised, no change can be made. The actual amount of converted terminal dividend through “Manual Lock-In Option” will be determined after the application is approved. The amount may be lesser or higher than the amount shown at the time when you submit your application. After the conversion of terminal dividend, your future terminal dividend will be reduced accordingly. Any terminal dividend that has not yet been converted can be higher or lower or reduced to zero. While the “Automatic Lock-In Option” is in force, the option will be immediately suspended upon partial surrender, and you have to submit a request to resume the option.

2. Changing the insured is subject to the prevailing administrative rules and shall not affect the units, policy values, policy date and policy year. The maturity date will be changed to the policy anniversary on or following the 128th birthday of the new insured. The new insured must be aged 65 years of age (last birthday) or below and must not be older than the initial insured by 10 years. The change of insured must be endorsed by the Policyowner, proposed new insured and assignee (if any). Both the new insured and the current insured must be alive and the policy is in force at the time the insured is changed and with satisfactory proof of evidence of insurability for the proposed new insured. We shall cease to provide any coverage for the Initial Insured or the prior insured on our record (when applicable and as the case may be) as from the Insured-Change Effective Date. Please refer to the policy provisions for details of changing the insured.

3. Upon the death of insured, if the Policyowner (still alive) and the insured is different person, the Beneficiary will become the new insured. If the Policyowner and the insured is the same person or the Policyowner died, upon the death of insured, the Beneficiary will become the new Policyowner and new insured of the policy, subject to the prevailing administrative rules of the Company. After this option has been exercised, all policy units, policy values, policy date and policy year will remain unchanged. Plan End Date of the basic plan of this Policy will be adjusted to the date of policy anniversary on the 128th birthday of the New Insured (in case the Policy Anniversary falls on the same date as the New Insured’s 128th birthday) or the immediately following policy anniversary. The policy value may be equal to or lower than Death Benefit before this option has been exercised. If the Death Benefit Settlement Option has already been selected, you shall cancel the Death Benefit Settlement Option arrangement before your submission of any written request for this Policy Continuation Option. Please refer to the policy provisions for details of Policy Continuation Option.

4. Additional Accidental Death Benefit only covers (i) death of the insured due to accident occurs in the first 8 policy years and the death occurs within 180 calendar days from the date of the accident; and (ii) after we received comprehensive and adequate proof of the accidental death of the insured. Additional Accidental Death Benefit up to 100% of total premiums paid (The minimum amount of Additional Accidental Death Benefit is equal to USD 15,000 per insured and the maximum amount is equal to USD 150,000 per insured.) This benefit is not available for the policy with Policy Continuation Option being exercised. Please refer to the policy provisions for details of Additional Accidental Death Benefit.

5. Total premiums paid refers to the total amount of premium(s) due and paid for the basic plan. If you partially surrendered this Policy, the total premiums paid will be proportionately reduced.

6. If the Policyowner opts for the beneficiary to receive “A lump sum payment for part of the Death Benefit and Additional Accidental Death Benefit (if any), and the remaining will be paid on a regular basis”, the lump sum amount should equal to or greater than 5% of the Death Benefit and Additional Accidental Death Benefit (if any). However, interest on unpaid Death Benefit and Additional Accidental Death Benefit (if any) is not guaranteed, therefore interest may be less than expected and the actual payout period may be shorter than the selected period. Only lump sum Death Benefit is applicable if an assignment is made. If the beneficiary(ies) die(s) while receiving the Death Benefit and Additional Accidental Death Benefit (if any) payments, the remaining amount will be paid to the beneficiary(ies)’ estate. If no beneficiary(ies) survives upon the death of the insured yet the Policyowner is still alive, the Death Benefit and Additional Accidental Death Benefit (if any) will be paid to the Policyowner in accordance with the Death Benefit settlement option. Policyowner may also request to receive the Death Benefit in lump sum. If the Policyowner dies while receiving the Death Benefit payment and Additional Accidental Death Benefit (if any), the remaining Death Benefit and Additional Accidental Death Benefit (if any) will be paid in a lump sum to the Policyowner’s estate. This benefit is not available for the policy with Policy Continuation Option being exercised. Please refer to the policy provisions for details of Death Benefit Settlement Option.

7. Upon full surrender, the Policyowner may choose to receive surrender payment in a fixed amount on a regular basis or increasing amount by installments. However, interest on unpaid surrender payment is not guaranteed, therefore interest may be less than expected and the actual payout period may be shorter than the selected or expected period. If the Policyowner dies while receiving the surrender payments, the remaining surrender payments will be paid in lump sum to the Policyowner’s estate.

8. Large Size Discount is only applicable to basic premium of Fortune Saver II (“Eligible Single Premium”). Other rider premium (if applicable) will not be entitled to the Large Size Discount. The Large Size Discount is on per Fortune Saver II policy basis. If customer has applied for more than one Fortune Saver II policy, all policies could enjoy Large Size Discount. However, the Eligible Single Premiums of the policies will not be aggregated in calculating the Large Size Discount Rate.

9. Annual dividend, terminal dividend and interest from accumulated annual dividend are not guaranteed. However, once distributed, the amount of the annual dividend and the accumulated interest will become guaranteed. An annual dividend may be payable at the sole discretion of the company on each policy anniversary. The amount of terminal dividend in each declaration may be greater or less than the previous amount based on a number of factors, including but not limited to investment returns and general market volatility.

10. The current interest rate offered is 2% p.a., but it is not guaranteed.

11. Worldwide Emergency Assistance Services are provided by International SOS Assistance (HK) Ltd. We reserve the right to change the terms and conditions of “Worldwide Emergency Assistance Service” and assumes no responsibility of the services provided by the third party service provider.

オフショア香港のFTLife社の商品のお申込みついて

FTLifeには香港でもっとも有名な保険会社。親会社は香港最大手の貴金属店の周大福やK11ショッピングモール、市バスなどを所有するNew World Development/新世界発展。つまり、香港を代表するコングロマリット(香港系財閥)の金融部門を担っている。2,800人以上のエージェントや独立した財務アドバイザーが在籍しています。

FTLifeの商品につき取り扱い商品

弊社取り扱いお勧め商品としては

- 積み立て資産承継貯蓄保険のRegent Insurance Plan 2 Premier

- 一括払い資産承継貯蓄保険のFortune Saver Insurance Plan Ⅱ

- 年金プランのIncomePro Annuity Plan

- 積み立て投信保険のOscar

- 一括支払い投信保険のLegend

- 積み立てリバース モーゲージ年金保険のOn Your Mind

| サポート内容抜粋 | 料金(HK$) |

|---|---|

| 商品のご案内 | 無料 |

| 住所や電話番号など各種変更手続き | 1,000/回 ※弊社の顧客は無料 |

| その他、各種手続きやトラブル解決や通訳 | お問合せください |

FTLife香港の基本情報 Fundamental information of FTLife Hong Kong

香港で最も知名度のある保険会社の一つです。アジア地域にグローバル金融サービスを提供しています。

世界の格付け機関から受けた推奨や高格付け(Fitch Ratings A-)は、F財務力の強さを表しています。FTLifeは多様な商品を提供し、将来設計や資産承継などあらゆる角度から顧客の資産をオフショアで保全します。

| 名称 | FTLife Insurance Company Limited / 富通保保険有限公司 又は単に FTLife |

|---|---|

| KOWLOON - FTL Prestige Service Centre | Suite 3106-09, 31/F, Tower 6, Gateway, Tsim Sha Tsui, Kowloon, Hong Kong |

| 営業時間 ※香港時間 | 月~金曜日: 9:00~19:00 土曜日: 9:00~13:00 |

| カスタマーホットライン/電話番号 | +852 2866 8898 |

| ホームページURL | https://www.ftlife.com.hk |

| csc@ftlife.com.hk | |

| 申請書等の送付先 | FTLife Kowloon Customer Service Centre 7/F NEO, 123 Hoi Bun Road, Kwun Tong, Kowloon, Hong Kong |